Here's one of the most stressful situations in real estate: you've found the home you want to buy, but your money is tied up in the home you still own. You can't comfortably buy the new one until you sell the old one — but if you wait to sell first, you risk losing the home you love, or ending up with nowhere to live in between.

This morning's June jobs report came in significantly weaker than expected — and unlike last month's hot report, this one actually pushed mortgage rates lower. If you're buying a home or watching rates, here's what happened and what it means for you. What the Jobs Report Showed The U.S. economy added just 57,000 jobs in June — well below the roughly 110,000–115,000 economists expected, and the slowest month of hiring since February. On top of the miss, the prior two months were revised down by a combined 74,000 jobs, which makes the labor market look softer than previously believed. This is essentially the opposite of the report we got a month ago, when the economy blew past expectations and rates jumped. One detail worth noting for anyone in the housing world: while construction added jobs overall, residential building construction actually lost positions in June — a small but real soft spot in the part of the economy closest to housing. A weak jobs report is generally good news for mortgage rates. When the labor market cools, it eases inflation pressure and revives the case for the Federal Reserve to cut rates rather than hike them. That takes some of the upward pressure off — which is exactly what we saw in the market's reaction this morning. The Unemployment Rate Dropped — But for the Wrong Reason Here's the part that seems contradictory at first: even though hiring came in weak, the unemployment rate actually fell to 4.2%. How can both be true? The answer is in the labor force participation rate, which dropped 0.3 percentage points to 61.5% — its lowest level in about five years. The unemployment rate didn't fall because more people found jobs — it fell (from 4.3% to 4.2%) because people left the workforce entirely and stopped being counted as unemployed. That's a soft signal underneath a headline that looks strong on the surface. For the Fed and the bond market, this reinforces the "cooling economy" read rather than contradicting it. A shrinking labor force alongside weak hiring is not a sign of strength — and the market treated it accordingly. How Rates Reacted Mortgage rates track the 10-year Treasury yield, which moves on the bond market's read of inflation and growth. On weak economic data, the 10-year typically falls — and it did. Following this morning's report, the 10-year Treasury yield slipped to 4.478%, and the national average 30-year fixed mortgage rate eased to around 6.6%. Not a dramatic move, but a move in the right direction for buyers — and a welcome change from the upward pressure of the past several weeks. Wondering what today's move means for your purchase? I follow the market in real time and can give you an honest read on where rates are and what your options look like. Book a free call. Book a free 15-minute call → Is This the Start of a Trend? One report doesn't make a trend — and that's worth saying plainly. A single weak jobs number, especially one distorted by falling labor force participation, isn't enough on its own to conclude that rates are headed steadily lower. It's one data point in a noisy series that gets revised, sometimes significantly, in the months that follow. It's also worth remembering the bigger backdrop. Just a couple weeks ago, the Federal Reserve signaled at its June meeting that its next move could be a hike, with markets pricing in a possible increase as soon as October. Today's weak jobs data pushes against that narrative — and with new Fed Chair Kevin Warsh, who was appointed with a mandate favoring lower rates, some economists think a soft jobs report could give him cover to pivot toward a cut sooner than the June dot plot implied. But there's a genuine catch keeping the Fed boxed in: inflation is still too high. Average hourly earnings rose 3.5% in June, still running below the most recent 4.2% inflation reading, and the Fed can't cut aggressively while inflation sits well above its 2% target. So even a rate-cut-inclined Fed chair faces real constraints. Geopolitical developments remain a wildcard on top of all this, capable of moving oil prices and inflation expectations in either direction on short notice. The honest read: today is a positive data point for rates, but the broader picture is still a tug-of-war. For the full context on the Fed's recent shift, see what the June Fed meeting means for mortgages. What Buyers Should Do The practical takeaway hasn't fundamentally changed, even on a good day for rates: If you're under contract and closing soon — this is a favorable moment to lock, since rates ticked down. Lock with a float-down option so you're protected if rates rise but can still capture further improvement if this cooling trend continues. At Fairway, the float-down is available at no additional cost, which removes the usual trade-off between certainty and upside. If you're still shopping — today's move is encouraging, but don't try to perfectly time it. A single report can reverse. Focus on your financial readiness and finding the right home; the rate can be refinanced later if this cooling trend turns into a genuine downtrend. For a full framework, see whether to lock your rate now or wait. The Bottom Line June's jobs report was weak — just 57,000 jobs against expectations near 115,000 — and the details underneath were soft too, with the drop in unemployment driven by people leaving the workforce rather than finding jobs. Bond yields fell in response, and mortgage rates eased to around 6.6%. For buyers, this is a positive data point after a stretch of upward pressure. But it's one report, not a trend, and the broader environment — a Fed leaning hawkish, geopolitical uncertainty — still cuts both ways. Watch cautiously, lock when it makes sense for your timeline, and don't let the noise pull you out of the market when the right home is in front of you. Want a straight read on what to do with your rate right now? I work with buyers across Massachusetts and 13 other states and watch the market every day. Book a free call and I'll give you an honest answer based on your situation. Book a free call → | Start my pre-approval → Nate Moghadam is a mortgage loan officer at Fairway Independent Mortgage Corporation, licensed in Massachusetts and 13 other states. NMLS #906770 | Company NMLS #2289. This content is intended for informational purposes only and does not constitute financial or investment advice. Mortgage rates change daily and vary based on individual borrower profiles and market conditions. This is not a commitment to lend. Contact a licensed loan officer to discuss your specific situation. Equal Housing Lender. Fairway Independent Mortgage Corporation Disclosures.

$500,000 is a real budget in Massachusetts in 2026 — but what it actually buys depends enormously on where you're looking. In some parts of the state, half a million dollars gets you a large, move-in-ready single-family home. In Boston proper, it gets you a condo, not a house. Understanding that geography before you start shopping saves a lot of frustration.

It's one of the most stressful moments in the homebuying process: you got pre-approved a few weeks ago, you were comfortable with where rates were — and then the market moved. Now rates are higher than when you started, and you're staring at a decision nobody prepared you for. Do you lock in now before they climb further? Or do you wait and hope they come back down?

The Federal Reserve wrapped up its June meeting today — the first under new Fed Chair Kevin Warsh — and the outcome matters for anyone buying a home or watching mortgage rates. Here's what happened and what it means for you. What the Fed Did The Fed held its benchmark interest rate steady, keeping its target range at 3.5%–3.75% — the fourth meeting in a row without a change. No surprise there. With inflation running at its highest level in over three years, a cut was never on the table for this meeting. The bigger news was in the Fed's updated economic projections — specifically the "dot plot," which shows where individual committee members expect rates to go. And the signal was clear: the Fed's next move is now more likely to be a hike than a cut. Of the 18 officials who submitted forecasts, nine projected at least one rate hike this year — and six of those nine penciled in multiple hikes. Only one official projected a cut in 2026, and one participant (presumably Warsh himself) didn't submit a forecast at all. The median forecast now shows rates ending the year at 3.8% — up from 3.4% in the Fed's March projections. Even more telling: after the meeting, markets moved up their expected timing for a hike. CME FedWatch data showed traders now pricing in roughly a 60% chance of a rate increase as soon as October — whereas before this week, they didn't expect a hike until December. The updated dot plot suggested committee members now expect to raise rates by a quarter percentage point this year. That's a significant turnaround from just three months ago, when the median committee member was projecting a quarter-point cut in 2026. The combination of a strong labor market and inflation at 4.2% has flipped the script. Why the Shift? Two things changed the Fed's calculus since their March projections: Inflation flared. The Iran conflict that began in late February pushed oil and gas prices sharply higher, driving the Consumer Price Index to a 4.2% annual rate in May — the highest since 2023. The labor market stayed strong. The May jobs report came in at 172,000 jobs added, more than double expectations. A strong labor market gives the Fed room to fight inflation without worrying as much about tipping the economy into recession. Together, those two factors have pushed rate cuts off the table and put a hike squarely into the conversation. Kevin Warsh's First Press Conference This meeting was notable as the first under new Fed Chair Kevin Warsh, who succeeded Jerome Powell. Warsh struck a notably hawkish tone on inflation, emphasizing that price stability is the Fed's priority. In his most pointed comment, he said the Fed "will deliver price stability" and called the commitment "strong, unanimous, and unambiguous." On the Fed's 2% inflation target, Warsh was emphatic that it isn't going anywhere until it's achieved. Asked whether he'd reconsider the target, he said: "The 'two' is the left of the decimal point. For now, 'zero' is to the right." In other words — with inflation at 4.2%, the Fed isn't even close, and there's no discussion of changing the goalposts until they hit it. Warsh also announced a significant overhaul of how the Fed operates, establishing five task forces to examine the central bank's communications, balance sheet, data sources, productivity and jobs analysis, and inflation frameworks. He revamped the policy statement to be shorter and simpler, and pointedly abstained from submitting his own projection to the dot plot — consistent with his long-stated skepticism of forward guidance. For markets, that communication style means less hand-holding about future moves and more emphasis on a data-dependent, flexible approach. In practical terms, that can mean more rate volatility around economic data releases, since the Fed isn't telegraphing its next move as clearly as it did under Powell. Wondering what this means for your specific situation? I follow the market daily and can give you an honest read on where rates are and what your options look like right now. Book a free call. Book a free 15-minute call → What This Means for Mortgage Rates Here's the important nuance most headlines miss: the Fed's benchmark rate doesn't directly set mortgage rates. Mortgage rates track the 10-year Treasury yield, which moves based on the bond market's expectations for inflation and growth — not the Fed funds rate itself. So while the Fed signaling a potential hike sounds alarming, the mortgage market reaction was relatively contained. The 30-year fixed rate has been hovering around 6.52%, just shy of 2026's high. On the day of the decision, the 2-year Treasury — which closely tracks Fed expectations — jumped about 11 to 14 basis points to near its highest level in over a year, while the 10-year (which drives mortgage rates) rose more modestly, up around 4 basis points to 4.469%. There was also a genuinely positive development working in the other direction this week: the U.S. and Iran reached an agreement to de-escalate, which sent oil prices lower earlier in the week and eased some of the energy-driven inflation fears. That pulled the 10-year down before the meeting — acting as a counterweight to the Fed's hawkish signal. The net result is a tug-of-war: a hawkish Fed pushing rates one way, easing oil prices pulling the other. The net effect: crosscurrents. A hawkish Fed pushing one direction, an Iran de-escalation pulling the other. That's why nobody can tell you with certainty where rates go from here. What Buyers Should Actually Do The practical takeaway hasn't changed much from the broader rate environment we've been in: If you're under contract and close to closing — locking makes sense. With the Fed signaling a potential hike and rate volatility likely to increase under Warsh's less-telegraphed communication style, the downside risk of floating is real. Lock with a float-down option if your lender offers one — at Fairway, the float-down is available at no additional cost, which means you're protected if rates rise but can still capture a lower rate if the Iran de-escalation pulls rates down before closing. If you're still shopping — don't let the Fed headline scare you out of the market. A potential quarter-point Fed move later this year changes your monthly payment far less than most buyers assume, and the bigger driver — the 10-year Treasury — is being pulled in two directions right now. Buying decisions should be based on your financial readiness and finding the right home, not on trying to time a Fed meeting. For a full framework on rate lock strategy, see when to lock your mortgage rate in 2026. The Bottom Line The Fed held rates steady in Kevin Warsh's first meeting but signaled its next move could be a hike — a clear shift from the rate-cut expectations of just a few months ago. Inflation at 4.2% and a strong labor market are driving that hawkish turn. For mortgage rates, the picture is more balanced than the headline suggests. The hawkish Fed is one force; the Iran de-escalation and falling oil prices are pulling the other way. The result is a market with no clear direction — which is exactly why locking with a float-down remains the smartest play for buyers who are ready to move. Don't try to time it perfectly. Focus on what you can control: your credit, your down payment, your loan structure, and being ready to act when the right home comes along. Want a straight read on what to do with your rate right now? I work with buyers across Massachusetts and 13 other states and watch the market every day. Book a free call and I'll give you an honest answer based on your situation. Book a free call → | Start my pre-approval → Nate Moghadam is a mortgage loan officer at Fairway Independent Mortgage Corporation, licensed in Massachusetts and 13 other states. NMLS #906770 | Company NMLS #2289. This content is intended for informational purposes only and does not constitute financial or investment advice. Mortgage rates change daily and vary based on individual borrower profiles and market conditions. This is not a commitment to lend. Contact a licensed loan officer to discuss your specific situation. Equal Housing Lender. Fairway Independent Mortgage Corporation Disclosures.

If you bought your home with less than 20% down on a conventional loan, you're almost certainly paying private mortgage insurance — PMI. The good news is that unlike FHA mortgage insurance, conventional PMI is temporary. With the right approach, you can get rid of it and lower your monthly payment, sometimes much sooner than you'd expect.

If you're buying a higher-priced home in Massachusetts, you've probably heard the term "jumbo loan" — and you may be wondering whether your purchase falls into that category, what it means for your financing, and whether it's something to avoid or embrace.

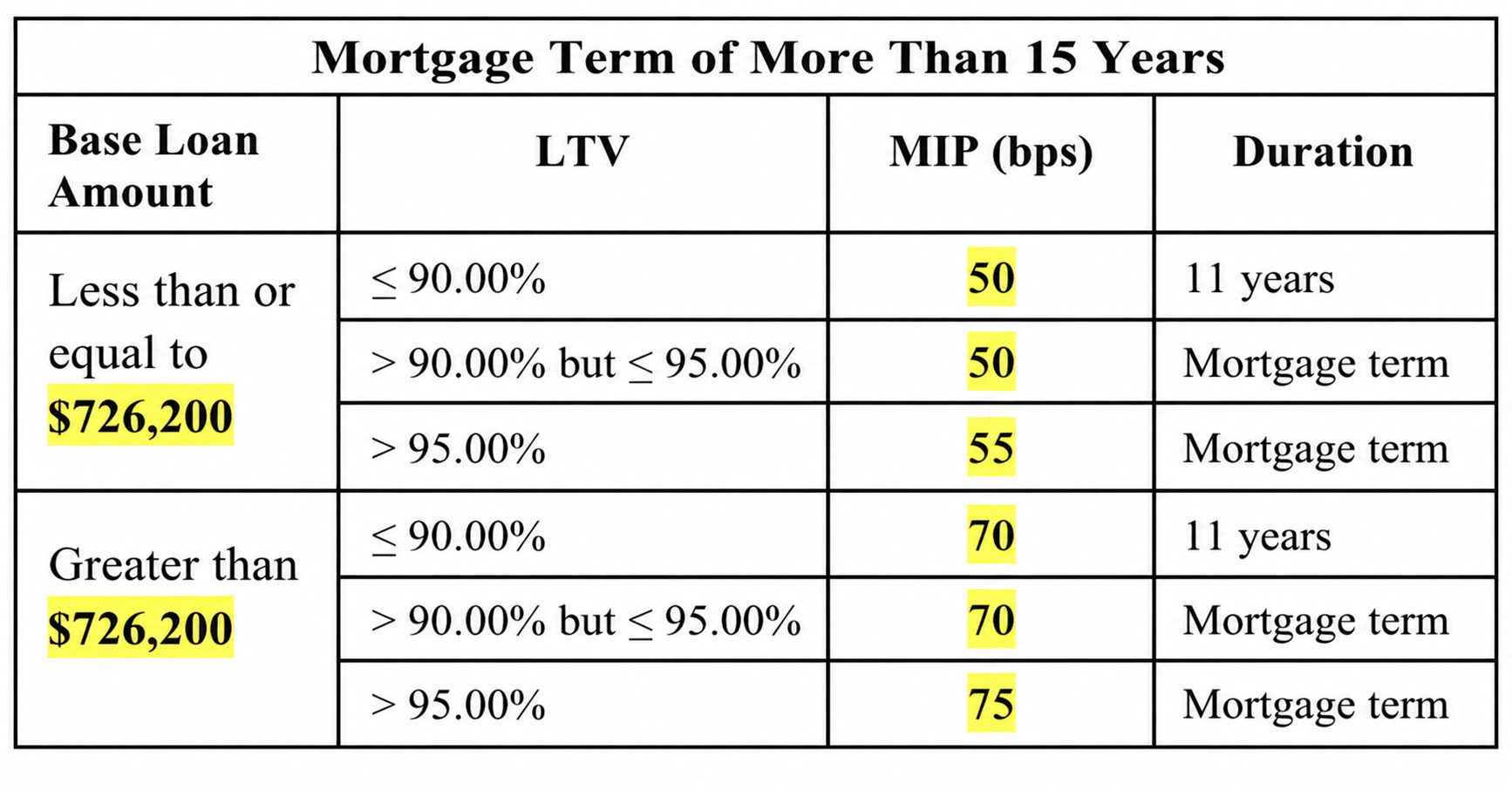

One of the most common questions I get from buyers considering an FHA loan is some version of: "How much extra am I actually paying for mortgage insurance?" It's a fair question — and the honest answer is more than most people realize when they're just looking at the rate.

This morning's May CPI inflation report came in hot — and if you're buying a home or trying to decide whether to lock a mortgage rate, here's what you need to know about what just happened and what it means for you. What the CPI Report Showed The Bureau of Labor Statistics reported this morning that the Consumer Price Index rose 0.5% in May on a monthly basis and 4.2% year-over-year — the highest annual inflation reading since 2023. Both numbers came in exactly in line with economist expectations. The one bright spot: core inflation — which strips out volatile food and energy prices — rose only 0.2% for the month, softer than the 0.3% consensus estimate, and 2.9% year-over-year. That suggests the inflation surge is being driven primarily by energy prices rather than broad-based price pressure throughout the economy. The headline number is still well above the Fed's 2% target. And it comes at a critical moment — the Federal Reserve meets next week, June 16-17, for the first meeting chaired by new Fed Chair Kevin Warsh. Why Rates Didn't Spike on the News Here's something worth noting: the 10-year Treasury yield barely moved after the report, sitting at 4.546% — essentially flat on the day. The national average 30-year fixed mortgage rate is currently around 6.67%, actually down slightly from Friday's close. Why didn't a hot inflation report push rates higher? A few reasons: The number was expected. Markets had already priced in a 4.2% reading. When data comes in exactly as forecast, there's no new information to react to. Core inflation was softer than expected. The 0.2% monthly core reading versus a 0.3% expectation gave the market a reason to breathe. It signals the inflation surge may be more energy-driven than structural. Much of this is already priced in. The rate market has been absorbing geopolitical risk, oil price spikes, and inflation concerns for weeks. Today's report confirmed the trend but didn't dramatically change it. The honest assessment: if mortgage spreads — the gap between the 10-year Treasury yield and the 30-year mortgage rate — were at their historical average rather than elevated levels, we'd easily be in the mid-7% range for mortgage rates right now. The fact that we're not is actually a relative positive for buyers. The Oil and Iran Factor Crude oil is up sharply today — WTI crude at $90.62, up 2.74%, and Brent at $93.70, up 2.46% — as Iran tensions continue to escalate. Oil prices are one of the primary drivers of headline inflation, which is why energy-driven CPI prints are being watched closely right now. The wildcard: if Iran tensions de-escalate meaningfully — a ceasefire, diplomatic agreement, or reduction in Strait of Hormuz supply disruption concerns — oil prices could fall sharply and take a significant portion of the inflation pressure with them. That scenario would be a meaningful positive for mortgage rates. Conversely, further escalation keeps oil elevated, keeps headline inflation hot, and keeps the Fed in a difficult position heading into their meeting next week. What the Fed Will Do The Federal Reserve is widely expected to hold rates steady at next week's June 16-17 meeting. Today's CPI report — while hot — was in line with expectations and doesn't change that calculus in the near term. What it does reinforce is the market's growing conviction that the next major Fed move will be a rate hike rather than a cut. Fed funds futures are currently pricing in a quarter-point raise at the December meeting. The combination of a strong labor market (172,000 jobs added in May) and inflation running at 4.2% gives the Fed little room to ease — and increasingly clear justification to tighten. For mortgage rates, a December rate hike is a relatively distant risk. The more immediate question is whether the 10-year Treasury yield — which drives mortgage rates more directly than the Fed funds rate — continues to drift higher as the market reprices for a longer period of elevated inflation. Not sure what today's rate environment means for your purchase? I'm watching the market in real time. Book a free call and I'll give you an honest read on where rates are and what your options look like right now. Book a free 15-minute call → What This Means for Buyers Right Now The immediate takeaway for buyers is actually more nuanced than the headline suggests. Yes, inflation is elevated. Yes, the Fed is leaning toward a hike before year-end. But today's rate reaction — essentially flat — suggests the market has largely absorbed this news already. A few things to keep in mind: Rates could still move in either direction from here. An Iran de-escalation or weaker consumer spending data could pull rates lower. Further oil price spikes or hotter-than-expected PPI data tomorrow could push them higher. The spread story is important context. At today's 10-year yield of 4.546%, mortgage rates "should" be closer to 6.0-6.25% based on historical spreads. They're at 6.67% because spreads are still elevated from post-2022 market stress. If spreads normalize, buyers benefit — without the Fed doing anything. Waiting for perfect rates remains a losing strategy. Buyers who've been waiting for rates to fall to 5% or 6% have watched home prices appreciate while they waited. The rate environment is what it is — the decision to buy should be based on your financial readiness and the right home, not a specific rate target. Should You Lock Today? If you're under contract and within 30-60 days of closing, today's data doesn't give you a strong reason to wait. Rates were essentially flat on the news, which means floating didn't cost you anything today — but the risk of rates moving higher on Thursday's PPI report or next week's Fed meeting is real. The best practice remains: lock with a float-down option if your lender offers it. That gives you rate protection against upside moves while preserving the ability to capture a lower rate if the market improves before closing. At Fairway, the float-down is available at no additional cost — which removes the typical trade-off between rate certainty and upside optionality. For a full framework on rate lock strategy, see when to lock your mortgage rate in 2026. And for context on last week's jobs report that set up today's inflation data, see what the May jobs report meant for mortgage rates. The Bottom Line May CPI at 4.2% is the highest inflation reading in three years — but the market already knew it was coming. Rates held steady because the data matched expectations and core inflation came in softer than feared. Oil prices and Iran tensions remain the biggest wildcard for where rates go from here. The Fed meets next week. PPI data drops tomorrow. Watch both. But don't let market uncertainty paralyze your homebuying decision — the buyers who win in this market are the ones who are prepared to move when the right home comes along, not the ones waiting for a rate environment that may never arrive. Want to talk through what this means for your specific situation? I work with buyers across Massachusetts and 13 other states and follow the market every day. Book a free call and I'll give you a straight answer. Book a free call → | Start my pre-approval → Nate Moghadam is a mortgage loan officer at Fairway Independent Mortgage Corporation, licensed in Massachusetts and 13 other states. NMLS #906770 | Company NMLS #2289. This content is intended for informational purposes only and does not constitute financial or investment advice. Mortgage rates change daily and vary based on individual borrower profiles and market conditions. This is not a commitment to lend. Contact a licensed loan officer to discuss your specific situation. Equal Housing Lender. Fairway Independent Mortgage Corporation Disclosures.

Finding the best mortgage lender in Massachusetts isn't about who has the lowest rate on a banner ad. It's about who can actually close your loan — on time, at the terms they quoted, without surprises after you're already under contract.

.jpg)